The Case For Hardware-Enabled Software

VC Copium

Much Ado About Moats

SaaS multiples have compressed under AI uncertainty, eroding terminal values. Median public SaaS are now trading at 3x NTM revenues & 14x NTM FCF1

Of Helmer’s 7 Powers, enterprise software has historically drawn defensibility from switching costs and for the fortune few, network effects

Switching costs in particular are under threat now computer-use agents can build API bridges around legacy systems of record and the disruptor playbook (ala Rox’s thesis in CRM) is to aggregate unstructured data upstream of the SoR & disintermediate. Enter the race to systems of action / systems of context or whatever your favoured coinage

Incumbents like Salesforce are reacting, opening up to MCPs and agent’s to disintermediate their UIs

The best founders starting today enter the market with enormous opportunity cost and some big looming questions:

Where does terminal value actually accumulate over a 5–10 year horizon?

Where can new switching costs be built that software alone cannot circumvent?

Hardware-enabled software (HES)

HES is a category of vertical software that anchors its intelligence in first-party data gathered by proprietary hardware the company deploys itself

Axon is a canonical example. Starting in 2001 as TASER International, they began purely selling ‘conducted-energy weapons’, then in 2008 layered in body cameras and crucially cloud-based evidence management, shifting the business to owning digital workflows. Now Axon, the company has aggressively bundled and subsidised hardware via free trials expanding into adjacent workflows like in-car video, interview room software, and integrated evidence tools making displacement increasingly difficult once embedded. In FY25 the results weren’t too bad, $2.8bn revenues,33% YoY growth, 125% NRR and a 62% blended GM across hardware and software.

More recently, Axon has moved to close the loop by automating labour within that workflow. Products like Draft One use generative AI to automatically produce police reports from body-worn camera audio, and the acquisition of Carbyne extends its footprint into emergency call handling and dispatch. The business has therefore evolved from:

selling hardware,

to selling hardware plus basic software,

to subsidising hardware in order to drive software adoption,

and ultimately to delivering hardware-enabled software that captures data in the field, processes it, and automates downstream tasks

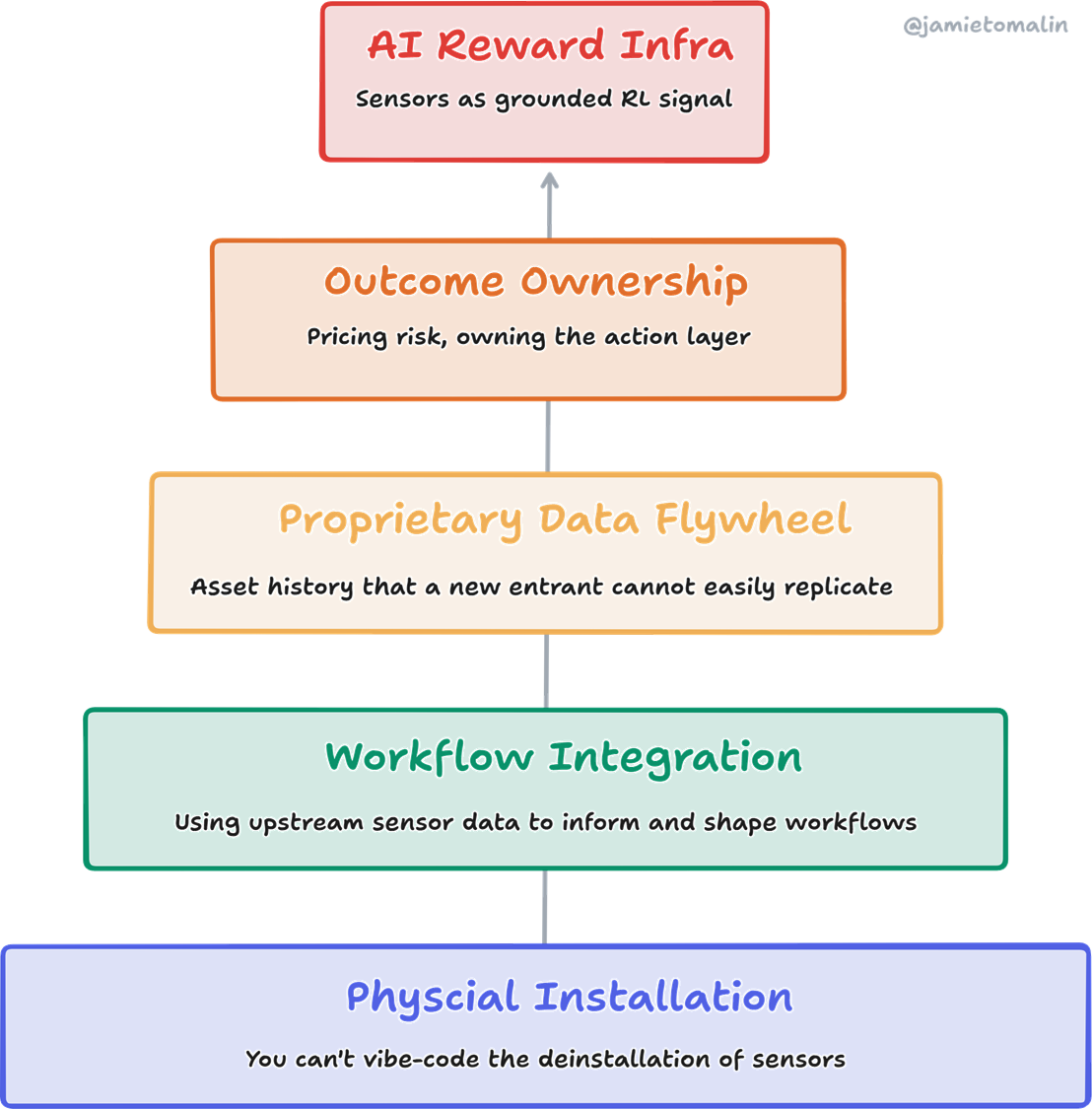

As the moats for traditional software erode, the argument emerges that physical sensing nodes out in the world (vision, lidar, radar, acoustics, thermal, motion etc) are the new scarce context

If you thought displacing Salesforce was hard, try displacing a sensor network after a CFO has signed off on capex and is depreciating the asset over 5 years. Or try fixing your John Deere. Once physically embedded in a workflow — mounted on a tractor, installed above a hospital bed, fitted to a vehicle — displacement requires physical intervention. In the lingua franca of X, one cannot vibe-code the de-installation of sensors.

In its best case, the retention logic extends into the elusive ‘data moat’. Subsidise or give away the device, embed it in a high-frequency operational workflow, use the data stream to automate decisions, and watch every new deployment expand a proprietary dataset that trains better models. Simples.

Unlike next-gen CRM plays that try to capture data upstream in the data warehouse, HES captures data at the point of physical origin enabling vendors to disseminated into downstream workflows. This is the classic system of record play, or in a world where your sensor output directly triggers an action, a system of action with an option on the ability to price outcomes, e.g. labour savings, loss reduction, uptime, insurance costs.

Pls,‘Why Now’?

But the coming of IoT has been called several times before with the internet, cloud, and 5G each cited as the decisive inflection. Each time, the physical GTM reality asserted itself. Selling into facilities, operations, and industrial settings is slow, relationship-driven, and requires on-site installation. Distribution constrained, the structural response was consolidation by serial acquirers like Halma who’ve spent decades buying distribution into sensor, analytics and diagnostic businesses. For de novo GTM approaches, have a number of structural shifts converged to create a ‘why now’?

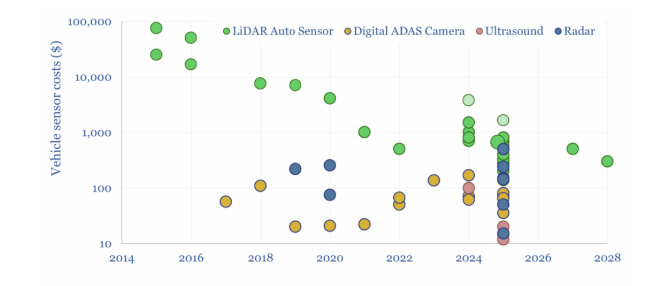

Hardware Keeps on Getting Cheaper

Hardware costs continue to come down, for instance LiDAR has deflated 90%+ in the last decade. This is perhaps unsurprising given it’s use in key tech Schelling points like Waymo’s autonomous cars. As Wright’s Law stipulates for every cumulative doubling in number of units produced, costs will decline by a consistent percentage. One can assume the robotics and physical AI boom will continue to power learning rates for the medium term, driving down associated sensor costs.

Falling sensor unit economics help to support new business models like ‘hardware-as-CAC’ whereby devices can be subsidised based on attached multi-year software contracts. A $100 GPS gateway attaching to a $20 p.m software fee has a 5 month payback. As the cost for edge-connectivity, sensors and hardware falls persistent coverage of large physical environments is now feasible.2

Expanding Sensory Menu

The range of economically viable phenomena that can be sensed is widening opening up the addressable market for start-up founders. The design space is enormous and creativity constrained. As ARIA put it: how do we deploy extremely multi-modal intelligent systems into the real world to reveal structures and patterns that exist but remain illegible?

Action is happening across AR devices, voice-first AI wearables, olfactory interfaces, neural interfaces, hyperspectral imaging, photonics, fauna? etc.

Analysis Cost Collapses and Agents Need Feeding

The prior IoT architecture (sensor → dashboard → human → action) always hit a ceiling of human bandwidth. Now, the argument becomes leveraging vision transformers and multimodal models to convert video and sensor data into embeddings (structured representations) that capture context, sequence, intent, and causality. Intelligence is no longer the bottleneck.

During the Anthropic <> Department of War brouhaha Dwarkesh’s CCTV cost calculation helped bring this and the feasibility of mass surveillance to life. The same logic can be applied to every domain where sensor data has been collected but not acted on (industrial, agriculture, health, infrastructure)

There are 100 million CCTV cameras in America. You can get pretty good open source multimodal models for 10 cents per million input tokens. So if you process a frame every ten seconds, and each frame is 1,000 tokens, you’re looking at a yearly cost of about 30 billion dollars to process every single camera in America. And remember that a given level of AI ability gets 10x cheaper year over year - so a year from now it’ll cost 3 billion, and then a year after 300 million, and by 2030, it might be cheaper for the government to be able to understand what is going on in every single nook and cranny of this country than it is to remodel to the White House.

@DwarkeshDavid Silver of DeepMind / Ineffable Labs fame outlines an additional bull case in his Welcome to the Era of Experience paper. As progress in supervised learning from human data slows, the bottleneck for next-gen AI agents will be grounded reward signals from the environment. Sensors are the reward infrastructure and whoever owns the sensor layer owns the training signal. As the limiting factor shifts from intelligence to data, availability and quality of sensor data becomes scarce. If agents require access to high-quality, real-time sensor streams does this create additional business models for incumbents & innovators? I would love to speak to anybody with an opinionated stance

Some HES Heuristics We’re Thinking About

Cheaper hardware lowers the decision friction but not the installation friction. Make the decision essentially zero-friction (free trial hardware, or so cheap it’s expensed), then build a deployment playbook that’s fast enough that installation friction doesn’t kill momentum. Axon’s free device trials, Dandy free intraoral scanners, Samsara’s self-install telematics, Genlog’s partnering with billboards. It’s perhaps unsurprising that lots of these players remain highly acquisitive, e.g. Badger Meter has made 9 acquisitions in the last 10 years, Axon at least 10

Time to value and asymmetry of being wrong. Time to value is always important. Ideally the customer sees something they couldn’t before within days, not months. Teton shows an anomaly in a resident’s overnight movement pattern in week one. Flock Safety can surface a plate match immediately upon deployment. Ideally one has an entry wedge that instruments a high-value, high-frequency decision workflow. Even better if the cost of a false negative in that workflow vastly exceeds the cost of the sensor system, e.g medical monitoring, structural integrity, security, critical infrastructure, predictive maintenance on essential equipment. There needs to be real asymmetry … if things go wrong, it’s very bad.

Workflow Expansion & Ownership. As we see from Axon, best in class HES seek to expand into multiple end-customer workflows and compound defensibility as every deployed device expands a proprietary dataset. AI-native vendors now also have the opportunity to close the loop so alerts trigger real work orders or fully automated actions (e.g. report writing, inspection, optimisation) rather than just death by dashboards.

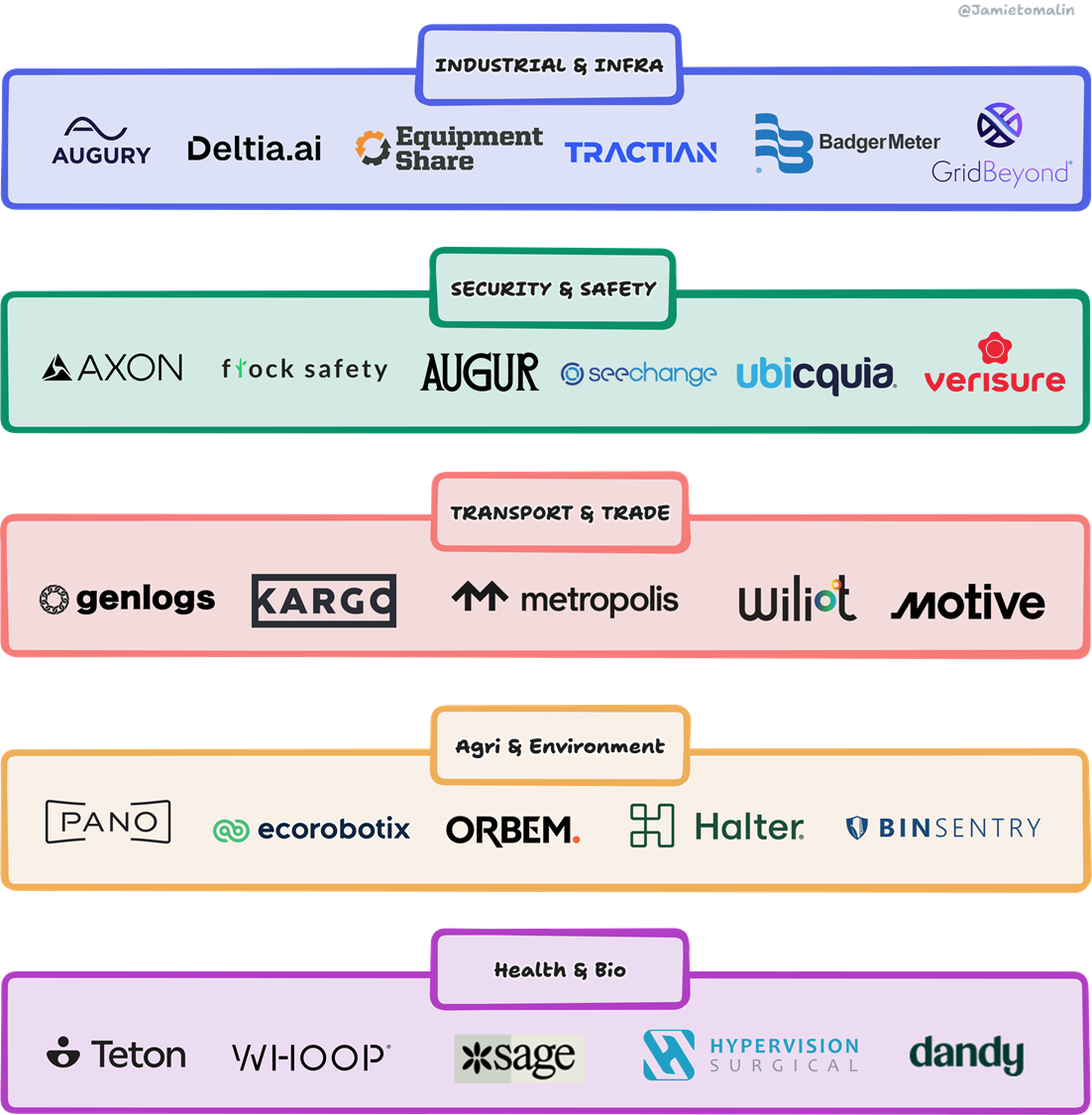

HES Market Map3

Below is a non-exhaustive list of innovators at the intersection of software and hardware we’ve founded interesting to study.

If you’re building at the intersection of hardware and software, or want to tell me why this is wrong, I’d love to chat on jamie@triplepoint.vc

As tech rotates into productive capitalism (energy, manufacturing, defence, robotics etc.) a new wave of vertical financing start-ups are emerging to support project planning and innovating on structuring, e.g. Odyssey, Tangible, Roebling, Cenotian. This is particularly key in hardware-as-a-service companies, like Evolv & Lumafield, where hardware is proprietary, capital-intensive, and the financing structure is central to the model. We’re excited by people innovating at this intersection

Industrial & Infra: Augury, Deltia, Equipment Share, LumaField, Tractian, GridBeyond, Badger Meter, Anybotics, AMP, Applied Computing Samotics

Security & Safety: Axon, Coram, Flock Safety, Augur, Ring, Verisure, Ubicquia, Cambridge Terahertz, SeeChange

Transport & Trade: Samsara, Motive, Genlog, Kargo, Metropolis, Wiliot

Agri & Environment: Orbem, Spore Bio, Ecorobotic, Halter, nofence, Binsentry, Matoha, SoFar, Pano

Health & Bio: Hypervision Surgical, Sage, Starlife, Inspiren, Tessan, Teton, Lilo Health, Whoop, Olden Labs, Dandy